Same GP. Same asset. Different games.

What Weinberg Capital Partners' first continuation fund reveals about the real state of French PE and what nobody is telling retail investors yet.

Hi all 👋

Before talking to Dimitri Fotopoulos, I hadn’t really measured what the shift means. A GP structuring a continuation fund around an asset he’s held for 5Y isn’t just extending a story. He completely changes his position with his LPs. Same investor, same asset and yet a completely different approach. A seller to those who want out, and a fundraiser with new investors who don’t know him yet.

Behind the clean mechanics Dimitri describes, there’s a question I’ve been asking myself for several months about this market : as continuation funds become structural in European PE, does everyone really understand what they’re investing in?

The 2025 figures make the question urgent. But first, the context because continuation funds weren’t born out of thin air.

European PE is looking for its exits

The question on every PE investor’s lips is: “How do you exit assets bought at pre-crisis prices, in an interest rate environment that has reconfigured everything?”

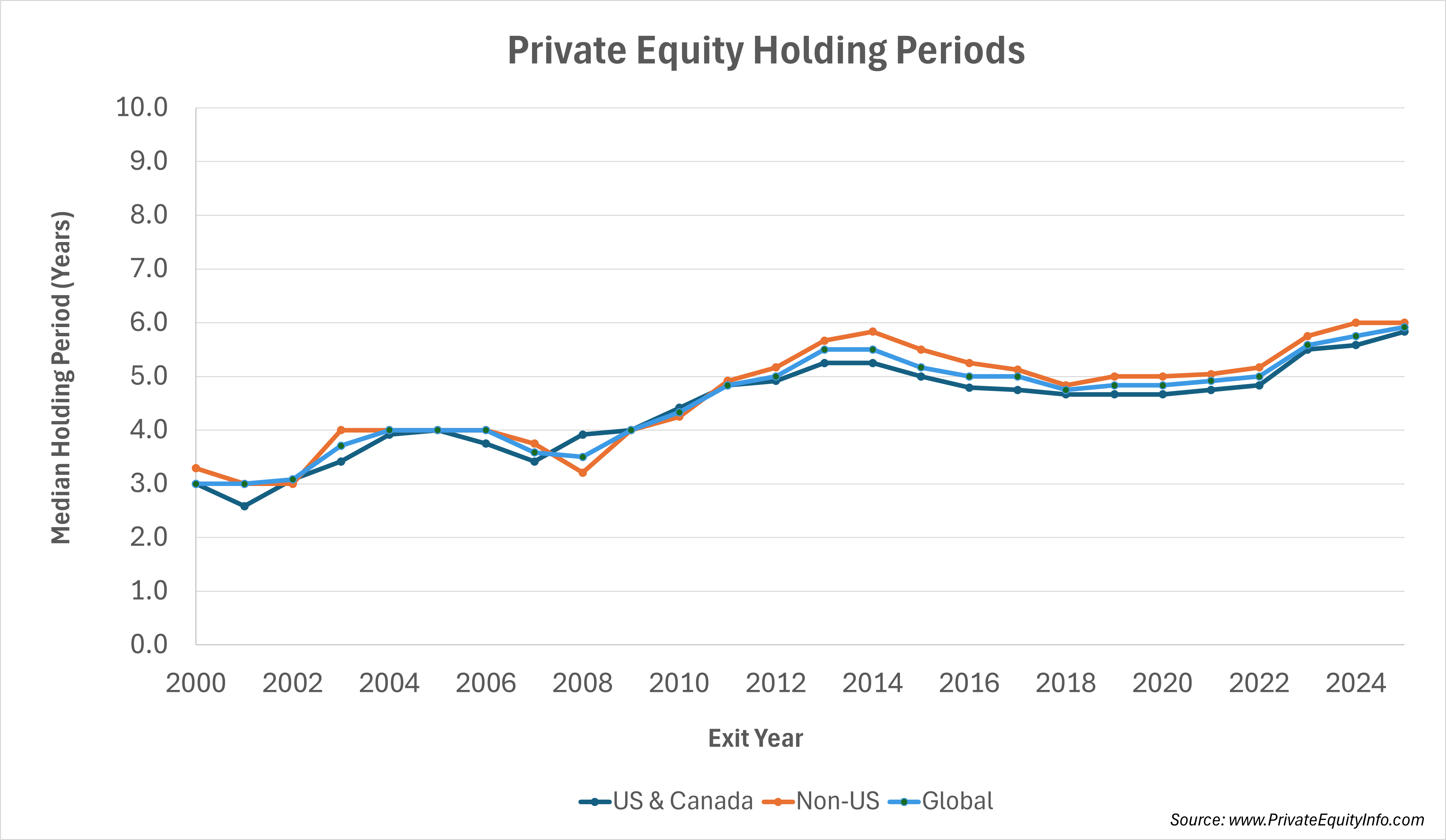

The median holding period for PE assets reached 7 years in 2025, a historical record. Bain specifies in its Global PE Report 2026 that for buyout funds, we’re hovering around 7 years, versus 5 to 6 years between 2010 and 2021. Nearly 40% of portfolio companies have been held for more than 5 years, up from 29% in 2019. The stock of unrealised assets represents today 32’000 companies and $3.8 trillion globally. It’s just huge !

We know it, 2025 still marked the beginning of a thaw. I looked at the figures and PE exits in Europe grew 5% in volume, with acceleration in the second half of the year. PwC puts the increase in exit value at +49% in 2025, to €272 billion. The Verisure IPO at €13.7 billion symbolised this reopening.

But the recovery remains selective and nobody should be surprised. What exits easily, as you’d expect, are TMT and financial services assets with solid earnings visibility. Industrials and consumer remain sluggish. And European fundraising in Q1 2026 fell back to €18 billion, from €23.7 billion a year earlier. The market is reopening, slowly, while LP pressure keeps building. It’s in this context that continuation funds stopped being a last resort tool and became more attractive funds in their own right.

The French figure that surprises

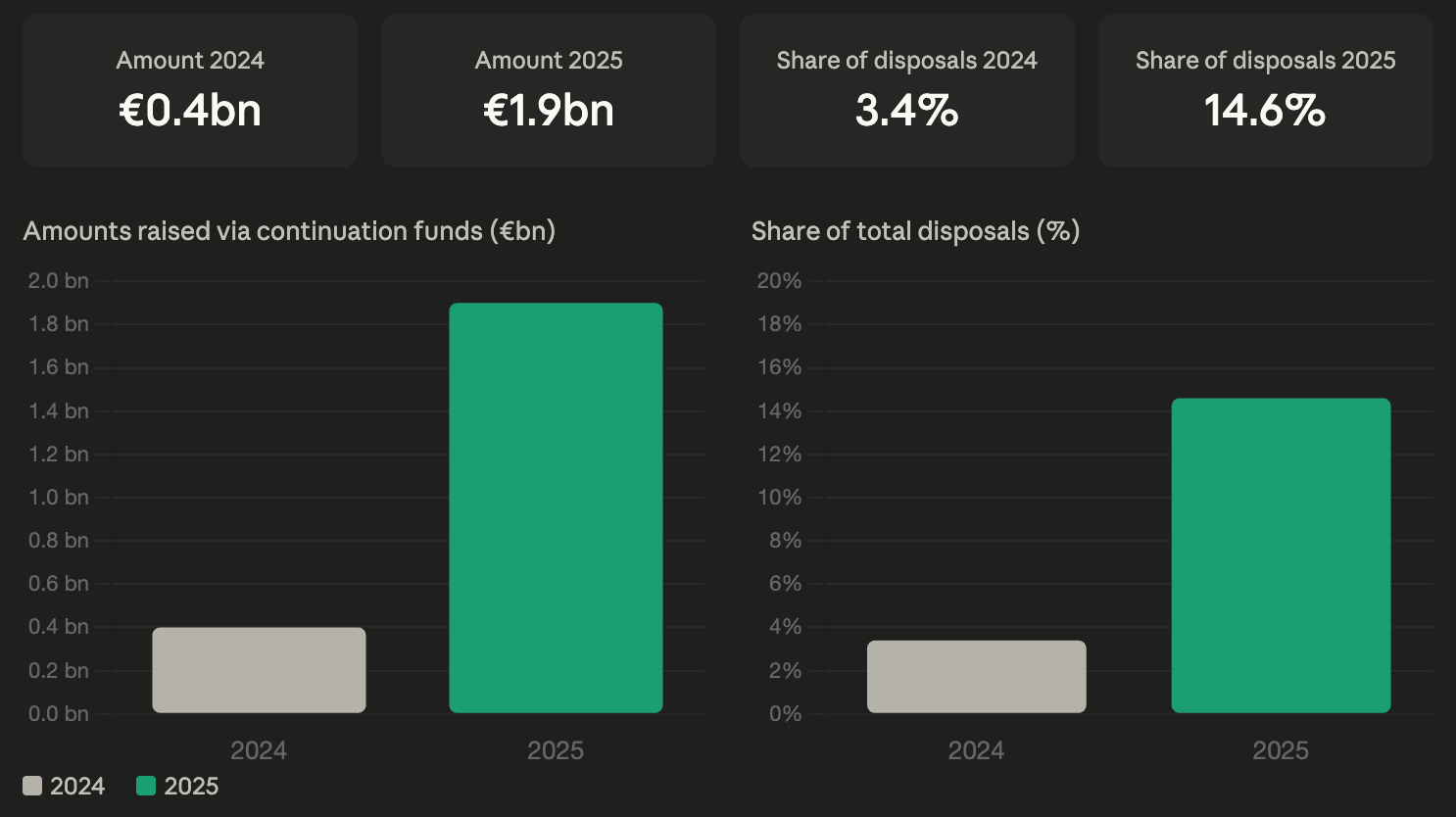

In France, continuation funds grew 4.75x in a single year. That’s not me saying it, that’s Dimitri. In 2024, they represented €400 million, or 3.4% of total disposals. In 2025, we reach €1.9 billion and 14.6% of disposals, according to the annual France Invest / Grant Thornton study of March 2026.

What these figures reveal beneath the surface is less a trend than a signal. Excluding continuation funds, French fundraising falls 2% in 2025. Disposal values rise solely because this tool exists. The average time to close a fund reaches 23.6 months, a 6Y record. This isn’t a market in difficulty rather a market that has found a clean emergency exit and is using it.

The quality of the “tool” depends entirely on the quality of the asset inside it. And that’s precisely why the mechanics matter and why we dwell on them in this conversation.

The real mechanics, from the inside

Dimitri has been a Partner at Weinberg Capital Partners since 2017, where he leads the mid-cap LBO strategy. In 2025, he structured WCP’s first continuation fund around Sapian, an asset that entered the portfolio in late 2019 via WCP3.

What struck me in this conversation is that the process is far more structured than you’d imagine. Three distinct sequences, in an order that can’t be reversed.

First, finding a lead investor among secondary market players. Several dozen in Europe today, highly professionalised, who analyse the asset and form an independent conviction. At WCP, Lazard accompanied the process to guarantee a fair price, established with a third-party valuation. This is where everything is decided: fund structure, regulations, valuation, management reinvestment.

The second consists of consulting the existing LPs. Each one chooses between receiving their liquidity in cash or continuing in the new fund. At WCP, a significant portion chose to stay, which Dimitri reads as a signal of conviction on the asset.

The third consists of syndicating with additional secondary investors to complete the round.

In a traditional process, the GP and the buyer barely speak before signing. Here, the secondary lead investor due diligences the management team as much as the asset itself. Two due diligences in parallel : the company and the GP.

The fee structure says the same thing differently. You go from 2% / 20% to approximately 1% / 10%, which brings the economics closer to a co-investment. The GP earns less in fixed management fees and bets more on the carried. Stronger alignment with investors, and more pressure to deliver on performance rather than on AUM.

What the models don’t measure

Bain specifies this in its 2026 PE Report : 58% of value creation in buyouts today comes from operational execution meaning the organisation’s capacity to deliver the plan. And operational execution depends on the teams, starting with the CEO.

I had already dug into this quite a bit with Bleuzenn Pech de Pluvinel, Senior Partner in charge of PE at Accenture, last year (episode here).

The fit between the GP and the CEO is fundamental. It’s a survival condition for the deal.

What I observe through my board mandates is that this conviction is built in the first conversations, in the way a CEO talks about their teams, in what they choose to say or not say. The mid-cap GPs with the best track records I know have all developed a form of human reading that appears in no investment memo.

The model predicts potential. The fit decides whether that potential will be reached.

Democratisation: pedagogy as the only way up

Dimitri mentions almost in passing that Weinberg CP has launched a dedicated wealth management initiative to make private equity accessible to a clientele that had no access to it until now. It’s a strong underlying trend across the market : ELTIFs, platforms like Caption or Moonfare, retail initiatives from major European GPs.

The logic is compelling and Long Term PE returns are real. But this underlying asset class is recent, still poorly understood and the market is already mixing the good and the less good without wealth distributors always having the tools to tell the difference. Dimitri himself is very cautious on the subject. A continuation fund on a single asset, without diversification, with a five year horizon and structurally limited liquidity, it’s a complex product. Not inherently dangerous, but complex.

What I’d say to GPs engaging in this direction is that the only way up isn’t regulatory, it’s pedagogical. Active clarity towards investors : on what’s being bought, on what can’t be promised, on the conditions under which this tool is virtuous and those under which it isn’t. That’s the only real safeguard. The market is democratising faster than the understanding of what it contains. Only GPs can close that gap.

Sources: Bain & Company Global PE Report 2026 - PwC Private Equity Trend Report 2026 - Roland Berger European PE Outlook 2026 - Private Equity Info, February 2026

After 350+ episodes, what I observe: my guests are driven by a fire. A conviction that things need to change, that finance can do better, that the tools exist. That is why Finscale exists - to aggregate those fires and make them audible to the people who make decisions. Six years. Do share it around you.